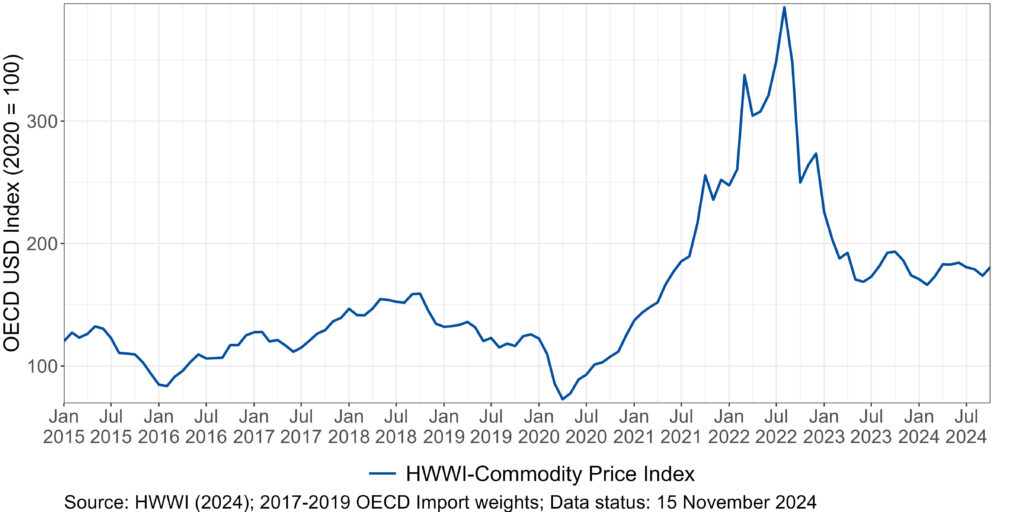

Hamburg, – 19. November 2024 – The HWWI-Commodity Price Index continued its downward trend from July in August and September, falling by -0.9% in August and -3.0% in September. In October, however, the index rose by 4.1% to 180.8 and is therefore -6.5% below the level of the same month last year (as of 15 November 2024).

The decline in the HWWI-Commodity Price Index during August and September was mainly driven by falling oil prices. A combination of abundant supply and weakening global demand led to the price drop, with China’s slowing economy playing a significant role. Additionally, the transition to renewable energy sources contributed to reduced demand for traditional fossil fuels.

In August, this trend was partly offset by a 19% increase in the European gas price index, which was 14% higher compared to the same month last year. This rise was driven by market turbulence, particularly concerns over supply disruptions due to the impact of Russia’s war on Russian pipelines, as well as unplanned maintenance in Norway. However, the situation was mitigated by well-stocked gas storage facilities, which helped to ease market tensions. Meanwhile, the US gas price index rose by 14.9% in September, largely due to the geopolitical instability in the Middle East, though it remained -11.2% below the level of the previous year. However, oil prices also rose in October due to tensions in the Middle East and rising demand as a result of colder temperatures, causing the HWWI-Commodity Price Index to rise. Overall, the index for energy raw materials fell by -0.2% in August and -4.6% in September and rose by 4.5% in October and was therefore -12.2% below the value for the same month of the previous year.

The food index also dropped by -4.2% in August, but rose slightly in September and October by 2% and 1.2% respectively. As a result, the food index was 14% higher in October compared to the same month last year.

In this area, prices for soya beans and soya bean oil fell particularly sharply. The index for soya beans dropped by -12% in August and was therefore -29% lower than in the same month last year. Similarly, the index for soya bean oil fell by -10.8% in August and was therefore -38% lower than in the same month of the previous year. This drop was primarily driven by ample supply, resulting from record harvests in Amerikca, paired with weak demand. Rice prices also followed a downward trend. The index fell by -10% in October, marking a -10.5% decrease compared to the same month last year. This was largely due to India resuming rice exports, prompting other producing countries such as Thailand and Pakistan to reduce their export prices. In contrast, sunflower oil prices moved in the opposite direction. Although the index saw a slight dip in August, it rebounded with increases of 1.8% in September and 12.6% in October, ending 32.5% higher than in the same month of the previous year. This rise was driven by strong demand, which was met with limited production from major producers Ukraine and Russia.

Coconut oil prices also rose significantly. The index climbed by 9.8% in August and 7.2% in September, before dropping slightly by -0.1% in October, still remaining 65% higher than the same month last year. The price increase was primarily caused by adverse weather conditions, including heavy rainfall and flooding in the producing countries. The price of palm oil continued its upward trend, with the index now 77.4% higher in October than in the same month last year. The price of sugar also showed an upward trend in September and October, rising significantly by 12% and 8.4% respectively, but was still -16.9% lower than in the same month last year. Pessimistic harvest prospects in Brazil and India’s decision to lift the ban on ethanol production from sugar cane were responsible for the sharp rise in recent months.

The index for industrial raw materials fell by -1.9% in August, but rose by 1.6% and 4.2% in September and October respectively and stood at 134.3 points in October, up 13.7% compared to the same month of the previous year. As in the previous reporting period, the price trend for iron ore stood out in particular. The index fell by -8.3% and -6.8% in August and September respectively, but rose by 14.1% in October, although it remained -10.6% below the October 2023 level. As in the last reporting period, a weak forecast for steel demand from China caused prices to fall at the beginning. The economic stimulus package announced by the Chinese government to support the construction sector led to a more optimistic outlook for demand and thus pushed prices up in October. Additionally, a supply shortage of zinc and aluminum in September and October contributed to rising index values. The aluminum index rose by 6.0% in October, though it was still -18.5% lower than the same month last year. The zinc index increased by 9.8% in October, 26.7% higher than in October 2023. These increases were primarily due to disruptions in exports from Guinea, a key producer of aluminium oxide. Furthermore, limited supply contributed to a rise in the wood index, which increased significantly by 10.4% in August and 7.6% in September. As a result, the index was 2.8% higher in October compared to the same month last year. The rubber index also reached record highs, marking its third-highest level in the past decade in October. Over the past three months, the index rose by an average of 6.9%, ending in October 42.6% higher than the same month last year. This increase was largely driven by adverse weather conditions in key production countries across Asia. Following extended droughts, heavy rainfall in Thailand caused flooding, while storms in China damaged large plantations. These weather disruptions led to lower production forecasts and, consequently, higher prices.

Source: www.hwwi.org