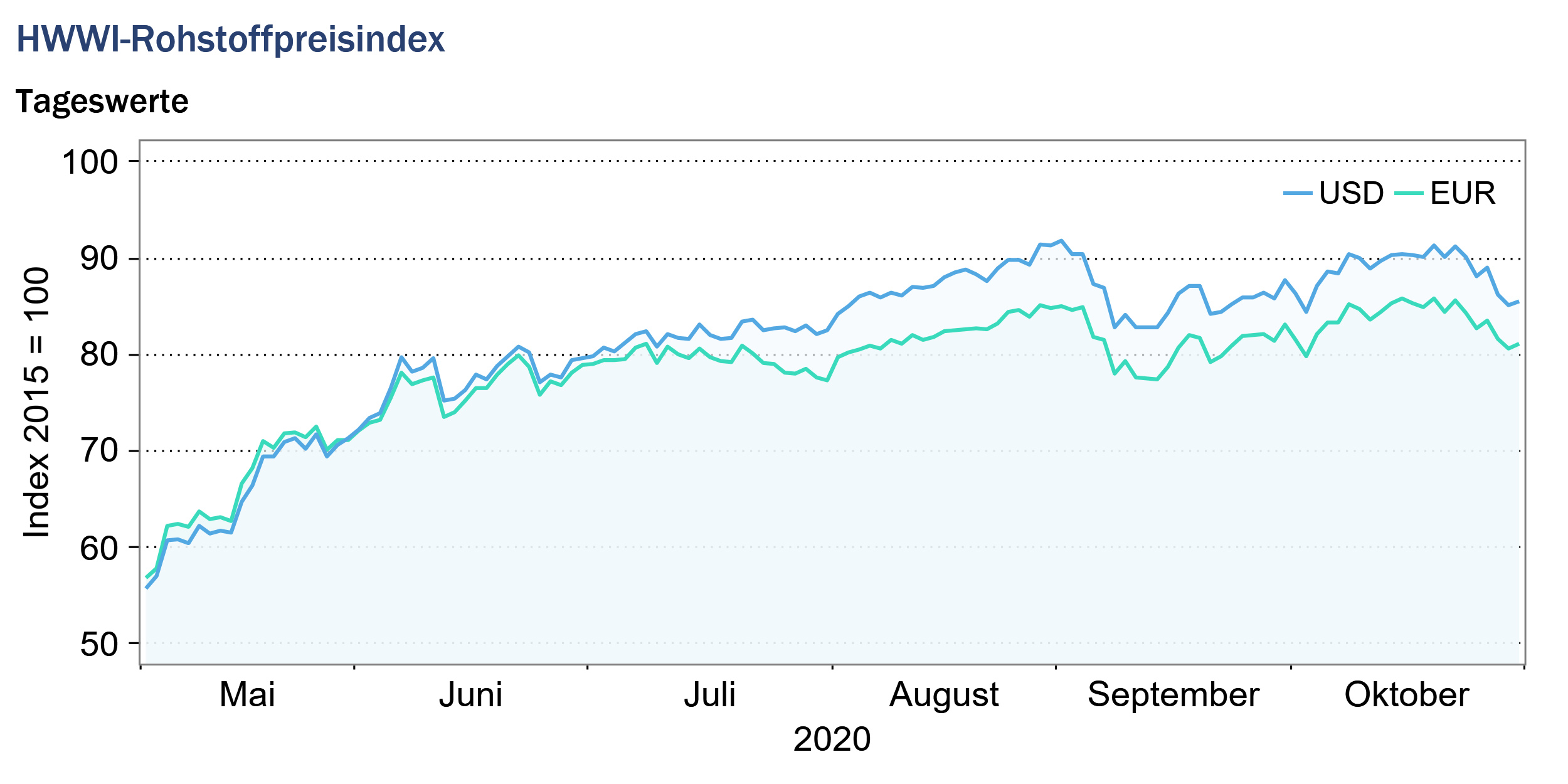

HWWI commodity price index increases slightly in October

- HWWI overall index rose by 3.1 % (US dollar basis)

- Crude oil prices fell by -0.7

- Grain prices increased by 7%.

(Hamburg, November 11, 2020) The HWWI commodity price index recorded a slight average increase in October compared to the previous month. Developments on the raw material markets were significantly affected by the rising corona infection figures in the USA and Europe, especially in the second half of October. The announcement of further lockdown measures in many European countries led to falling prices on the crude oil markets in the second half of the month. The second wave of the corona pandemic in Europe and the USA clouded the outlook for the global economy, but has so far had only a slight impact on prices for industrial raw materials. Due to the continuing increase in demand from China, prices, especially for industrial metals, remained at a high level. Significant price increases could be observed on the markets for food and beverages in October.

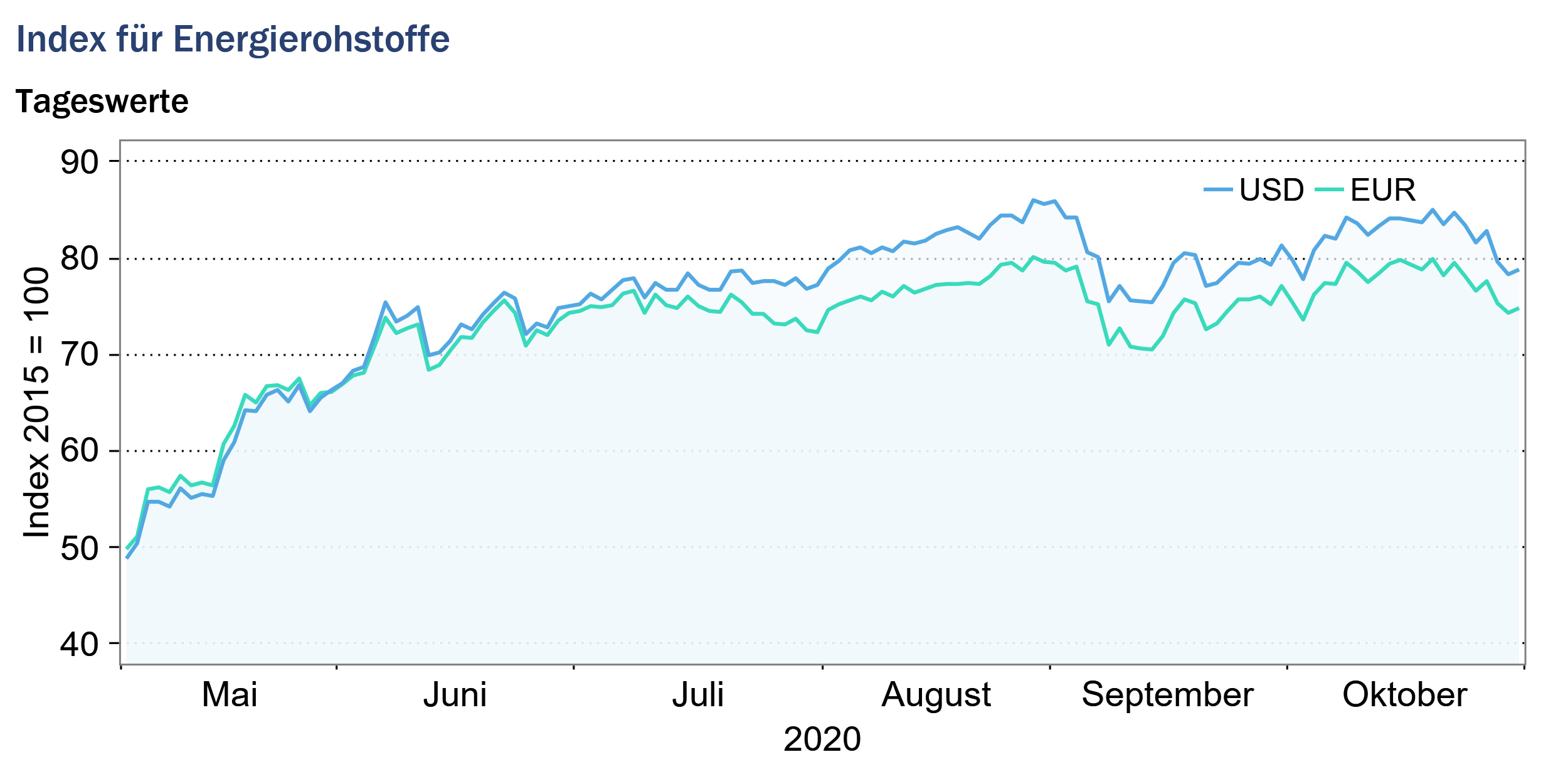

Index for energy raw materials: +3.8% (Euro basis: +3.9%)

After crude oil prices initially rose slightly at the beginning of October, the prices of all three crude oil types included in the index fell in the second half of the month and, at the end of the month, were only slightly above USD 37 per barrel for the European reference grade Brent and USD 35 per barrel for the American reference grade WTI. The renewed sharp rise in corona infection figures in the USA and also in Europe and the announcement of further lockdown measures in many European countries clouded the outlook for the global economy and led us to expect a further drop in demand for crude oil.

In addition to the demand burdened by the corona crisis, an expansion of supply in October put pressure on crude oil prices. On the one hand, the North African country Libya, which has been in civil war for years, announced that it would again significantly increase its own production volume. Oil production in Libya has been blocked by rebels for several months and has been under the control of the state oil company National Oil Corporation (NOC) again since October. On the other hand, Iraq again exceeded the production cuts agreed by OPEC+ in October and produced above the agreed limit.

A new meeting of the members of OPEC+ including Russia is planned for the end of November to discuss an extension of the production cuts. In view of the continuing weak demand and the expansion of crude oil production from non-OPEC countries, a mere extension of the easing is unlikely to be sufficient to sustainably support crude oil prices. It remains to be seen whether Saudi Arabia will be able to push through an additional cutback in production volume within OPEC+.

European and American natural gas prices rose sharply on a monthly average compared with the previous month. The approaching winter and rising natural gas consumption in private households due to output restrictions drove up natural gas prices in October. The U.S. Energy Information Administration estimates a 5 percent increase in U.S. natural gas consumption compared to winter 2019, due to expected colder temperatures and additional heating requirements due to curfew restrictions.

South African and Australian coal prices also saw an average increase in October compared to the previous month. The price of Australian coal rose on average by more than 10% compared with the previous month, but is still well below the level of the previous year’s month.

Overall, the sub-index for energy raw materials rose by 3.8 % (Euro basis: +3.9 %) to 82.3 points (Euro basis: 77.5 points).

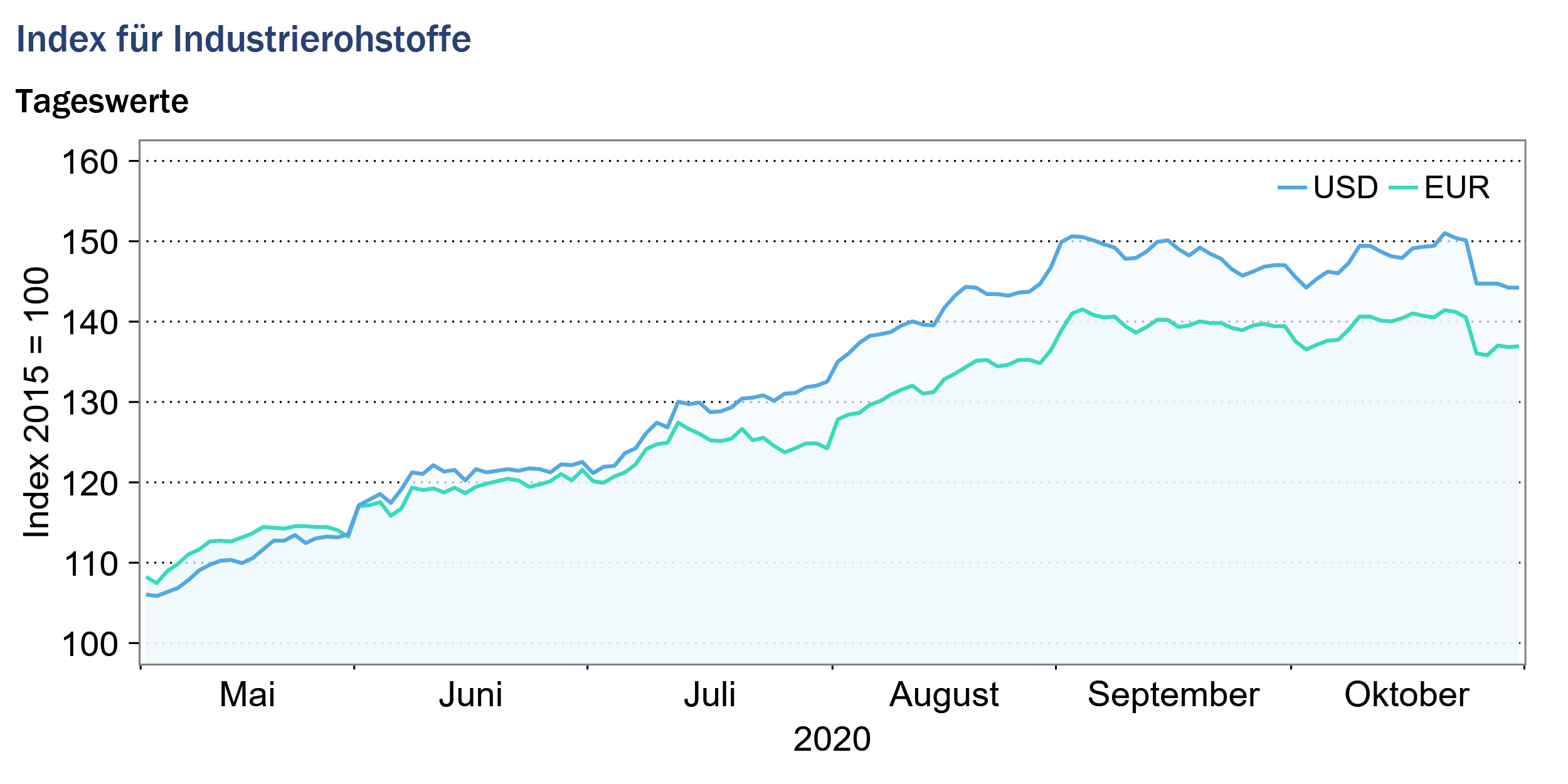

Index for industrial raw materials: -0.8% (Euro basis: -0.7%)

The sub-index for industrial raw materials is divided into the index for agricultural raw materials, the index for non-ferrous metals and the index for iron ore and steel scrap.

The upward trend in the prices of base metals, due to increasing demand from China, slowed down, or was interrupted for some base metals in October. While the Chinese economy continued to recover, the sharp rise in the number of infections in Europe and the US increased market uncertainty and depressed the prices of base metals. Especially in the second half of the month, when renewed lockdown measures were announced in many European countries, the growth of base metal prices slowed down or even resulted in slight price losses.

Thus, copper prices, driven by demand from China, still recorded increases in the first half of the month, but fell slightly in the second half of October. Nevertheless, copper prices remained at a high level, averaging 16.6 % above the average price in October 2019.

Iron ore prices also fell on average in October, down 3.7% from the previous month. The aluminum and nickel markets continued to show rising prices in October. Nickel prices in October continued to be driven by rising demand from Chinese stainless-steel production.

Australian wool prices recovered after the price low in September and benefited from rising demand from China. However, after an increase of over 16% compared with the previous month, average October prices are still 24.6% lower than the corresponding figure for the prior-year month.

Overall, the index for industrial raw materials fell on a monthly average by -0.8% (euro basis: -0.7%) to 147.4 points (euro basis: 139.0 points).

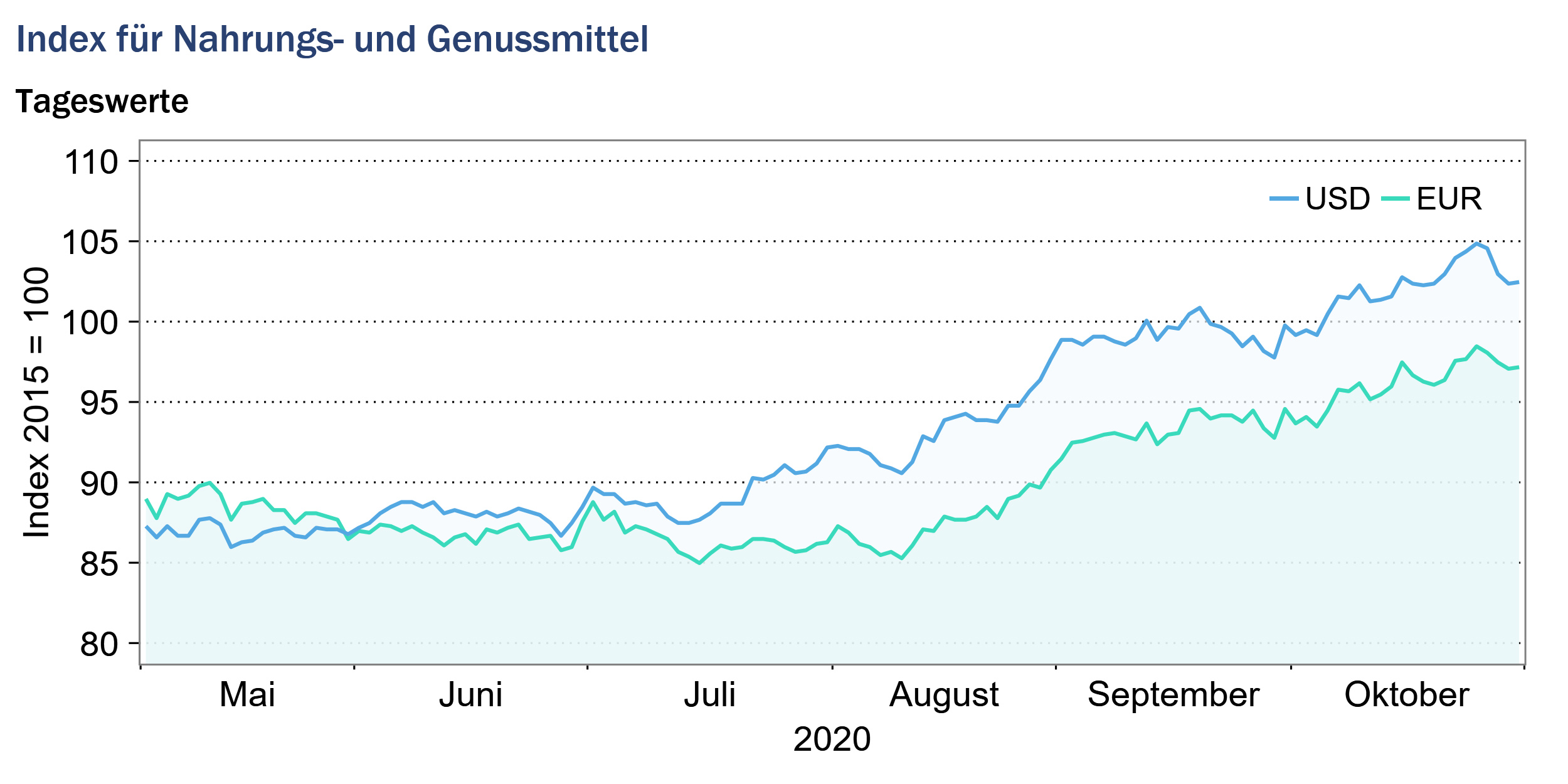

Index for food and beverages: +2.9% (Euro basis: +3.1%)

In October, prices for food and beverages continued to rise, mainly due to the sharp price increases on the grain markets. In particular, prices for wheat and barley increased significantly in October, rising by an average of over 12% compared to the previous month. Compared to the previous year, the average price for barley in October was 17% higher than in the same month of the previous year and the price for wheat was even higher than 30%.

As the corona crisis worsened, global export demand for grain increased in October, while supply decreased due to poor growing conditions in Argentina and continued drought in other major harvesting regions. Corn prices also rose, reflecting the strong increase in demand from China.

The markets for semiluxury food and beverages showed opposing trends in October. While sugar prices increased, coffee and cocoa prices decreased on average compared to September. The price increase in the sugar markets reflected the prospects for lower sugar production due to below average rainfall in Brazil and India. India and Brazil are the two largest sugar producers in the world. Sugar production in Thailand has also declined this year due to persistent drought, which further supports the sugar price. The price declines in the coffee and cocoa markets reflect a decline in global demand. The worldwide social distancing measures, which have recently been tightened again in many countries, have led to a collapse in demand for coffee and cocoa-containing products. Recently imposed contact restrictions and increased work from the home office have led to a decline in out-of-home sales of coffee and chocolate.

Overall, the index for food and beverages rose by 2.9% on a monthly average (Euro basis: +3.1%) and stood at 102.1 points (Euro basis: 96.2 points).

Source: www.hwwi.org